Description of Fiscal Items on the Local Finance Dashboard

- Last Updated:

Table of Contents

- List of financial items

- Organization Basic Information

- General

- Financial indicator

- Revenue

- Expenditures (by purpose)

- Expenditures (by type)

- Contact Information

- Related Information

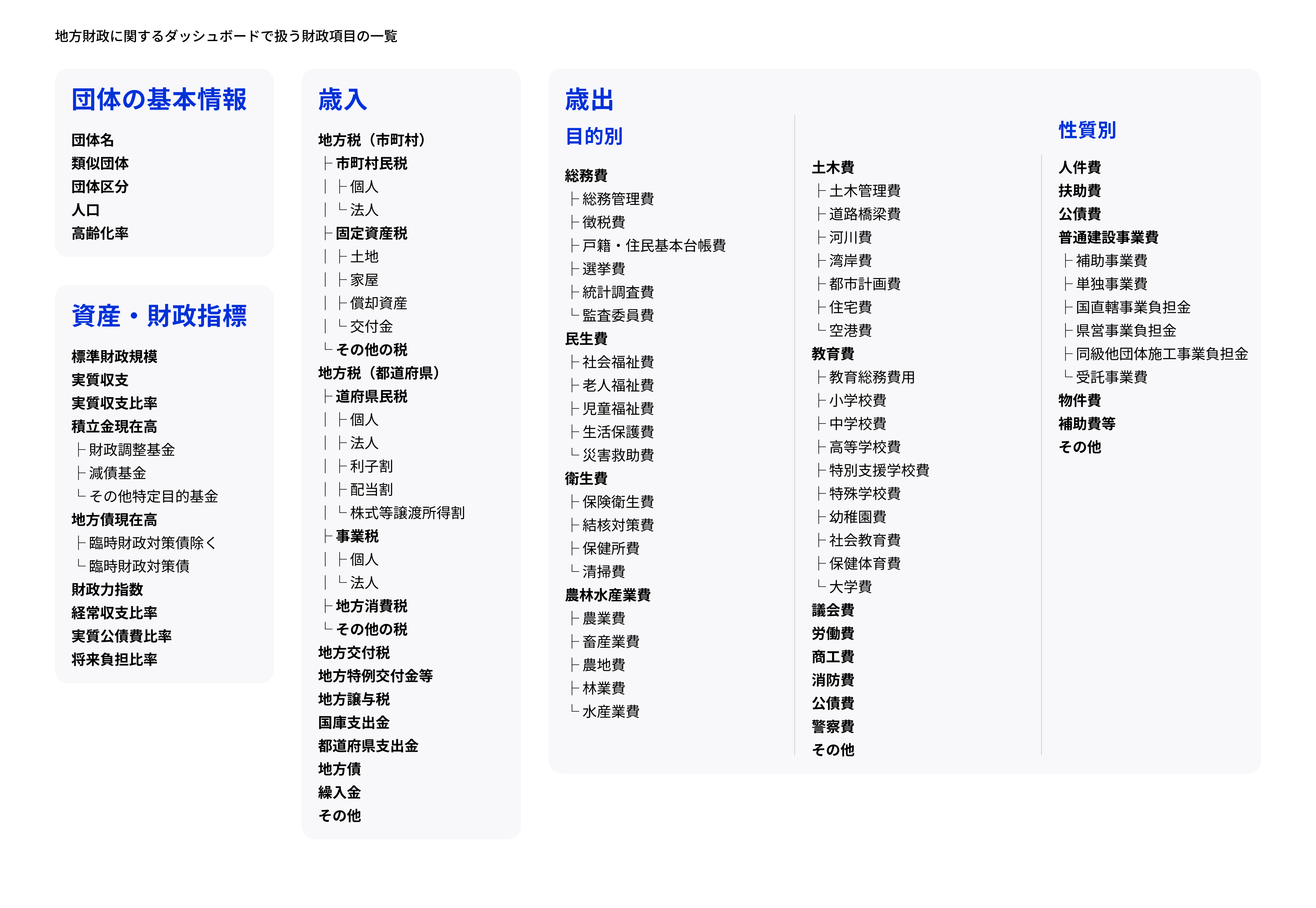

1. List of Financial Items

The dashboard on local public finance covers a breakdown of key items of revenue and expenditure, as well as key items of accounting and fiscal indicators.

Definitions of each item are excerpted from the 2026 Local Government Finance White Paper and the Ministry of Internal Affairs and Communications website.

2. Basic Information on Organizations

2.1 Similar Organizations

- State /

- Organizations that belong to the same type as the organization in question as a result of the classification of prefectures nationwide into five groups and Tokyo based on the financial capability index.

- City

- An organization that belongs to the same type as the organization concerned as a result of classifying municipalities nationwide into 35 types according to population and industrial structure.

The figures for similar organizations for financial indicators and revenues and expenditures (including their breakdown) indicate the average figures for similar organizations.

2.2 population

Based on the population recorded in the Basic Resident Register as of January 1 of the fiscal year under review.

2.3 Aging rate

Based on the ratio of the population aged 65 or older to the population on the Basic Resident Register.

3. General

3.1 Amount per person

The value of each indicator divided by the population.

3.2 Year-on-year change in value per person

Previous year's amount per capita = (amount per capita in the fiscal year - amount per capita in the previous year) / amount per capita in the previous year × 100

3.3 Average

3.3.1 Similar Organizations

The average value of each indicator by the selected local governments in each category. The selected local governments are those selected based on such criteria as the absence of large-scale mergers and the absence of extremely large deficits, as municipalities that conduct standard financial operations.

3.3.2 In the case of voluntary organizations

Value obtained by dividing the total value of the indicator for the selected organization by the number of organizations

4. Financial Indicators

4.1 Standard Financial Scale

This indicates the scale of ordinary general revenue resources that would normally be received under the standard conditions of local governments. It is the amount obtained by adding the ordinary local allocation tax to the amount of standard tax revenue, etc. Note that, pursuant to the provisions of the supplementary provisions of the Order for Enforcement of the Local Finance Act (Cabinet Order No. 267 of 1948), it also includes the amount of bonds that can be issued for extraordinary fiscal measures.

4.2 Real Balance

The actual difference between income and expenditure that should belong to the fiscal year. This is the amount obtained by deducting from the formal balance of payments financial resources such as continuing expenses carried over to the following fiscal year (gradually carrying over the remaining amount of continuing expenses executed each fiscal year to the final continuing fiscal year) and carry-over of approved expenses carried over (carrying over to the following fiscal year, in accordance with the provisions of the budget, of expenditure budget expenses for which expenditure is not expected to be completed within the fiscal year due to its nature or reasons after the budget is established).

Normally, "organizations in the black" or "organizations in the red" are judged based on the real balance of surplus or deficit.

4.3 Real income and expenditure ratio

The ratio of the real balance to the standard fiscal scale (including the amount of extraordinary financial countermeasures bonds that can be issued). A positive real balance ratio indicates a real balance surplus, and a negative real balance ratio indicates a real balance deficit.

4.4 Reserves

Expenses for funds established to maintain property or accumulate funds for a specific purpose.

4.4.1 Fiscal Adjustment Fund

Fund to adjust the imbalance of financial resources between fiscal years in local governments.

4.4.2 Sinking Fund

A fund established for the purpose of accumulating funds to systematically repay municipal bonds.

4.4.3 Other Special Purpose Funds

A fund established to maintain property and set aside funds for a specific purpose other than that of a fiscal adjustment fund or sinking fund. Specific examples include funds for the construction of government buildings, etc., funds for the enhancement of social services, and disaster response funds.

4.5 Local Government Bonds

Borrowings from the general account of local governments.

4.5.1 Extraordinary Financial Measures Bonds

Local government bonds issued as an exception to Article 5 of the Local Finance Act to be used for expenses other than investment expenses in order to deal with shortages in local general revenue resources. The national and local governments divide the amount of the regular revenue and expenditure revenue shortfall excluding revenue source countermeasure bonds, etc., equally. The national share is supplemented by transfer from the general account to the special account for local allocation tax (addition to extraordinary fiscal measures), and the local share is supplemented by extraordinary fiscal measure bonds. The amount equivalent to the principal and interest redemption of extraordinary fiscal measure bonds shall be included in the standard financial requirements for local allocation tax in subsequent fiscal years.

4.6 Financial Capability Index

This is an index that indicates the financial strength of local governments, and is the average value of the past three years of values obtained by dividing the standard fiscal revenue by the standard fiscal demand.

The higher the financial capability index is, the larger the retained financial resources for calculating the regular local allocation tax are, and it can be said that there is room in the financial resources. However, the financial capability index of special wards was calculated based on the standard financial demand amount and the standard financial revenue amount required to calculate the special ward financial adjustment grants.

4.7 Current Account Ratio

This is an indicator for judging the flexibility of the financial structure of local governments. It is the ratio of the amount of general revenue resources appropriated to expenses (ordinary expenses) that are regularly disbursed each fiscal year, such as personnel expenses, subsidy, debt service, etc., to the total amount of general revenue resources (ordinary general revenue resources) that are regularly received each fiscal year, mainly local taxes and ordinary local allocation tax, special treatment of revenue reduction compensation bonds, and extraordinary financial countermeasure bonds.

This indicator shows the extent to which ordinary general revenue revenue is allocated to ordinary expenses. The higher the ratio, the more rigid the financial structure.

4.8 Real debt service ratio

The average of the ratio of the effective amount equivalent to public debt service expenses * 1 pertaining to principal and interest redemption money borne by the general account, etc. of the relevant local public entity and quasi-principal and interest redemption money such as transfer for redemption of public enterprise bonds against the amount based on the standard fiscal scale * 2 for the past three years.

It can be said that it is an index of the size of the repayment amount of borrowings (local government bonds) and the equivalent amount, and shows the degree of impact of these on fiscal management.

The real debt service ratio under the Act on Financial Soundness of Local Governments is the same as the real debt service ratio under the Local Finance Act (Act No. 109 of 1948), which is used to determine which organizations require consultation for bond issuance and which require permission.

* 1 Total amount of principal and interest redemption (excluding advanced redemption, etc.) and quasi-principal and interest redemption, less specified financial resources appropriated thereto and the amount included in standard financial requirements related to principal and interest redemption, etc.

* 2 The amount obtained by deducting the amount included in standard financial requirements related to principal and interest redemption, etc. from the standard financial scale.

4.9 Future Burden Ratio

Ratio of the actual liabilities * 1 to be borne by the general account, etc. of a local public entity in the future to the amount * 2 based on the standard fiscal scale, including those related to public enterprises, local public corporation, and investment corporations, etc. that provide loss compensation.

The current outstanding balance of borrowing (local government bonds) of the general account, etc. of local governments and the burden that may be paid in the future, etc. is indexed, and it can be said that it is an index that shows the degree of the possibility of pressing the future finance.

* 1 The amount obtained by deducting the appropriable financial resources, etc. such as the amount included in the standard financial requirements related to the fiscal adjustment fund and principal and interest redemption, etc. from the future burden amount of the general account, etc.

* 2 The amount obtained by deducting the amount included in standard financial requirements related to principal and interest redemption, etc. from the standard financial scale.

5. Revenue

5.1 GENERAL RESOURCES

The total amount of local taxes, local transfer tax, special local grants, and local allocation tax. In addition, the total amount of the following is also included: Municipal tobacco tax prefectural grants received from municipalities; interest-based grants, dividend-based grants, stock transfer income-based grants, separate taxable income-based grants (only for ordinance-designated cities), local consumption tax grants, golf course use tax grants, automobile acquisition tax grants, automobile tax environmental performance-based grants, Diesel Oil Delivery Tax grants (only for ordinance-designated cities), and corporate enterprise tax grants received from municipalities. These grants are deducted as overlapping amounts between prefectures and municipalities in the net amount of local public finance.

5.2 General revenue resources, etc.

The sum of general revenue resources and revenue resources that, like general revenue resources, cannot be specified for use and can be used for any type of expense. This includes donations for unspecified purposes, property income sold for unspecified purposes, and bonds issued for extraordinary fiscal countermeasures.

5.2.1 Local allocation tax

A tax to be allocated by the national government to local governments for the purpose of balancing local financial resources and ensuring the planned operation of local administration without undermining the autonomy of local governments. Of the national taxes, a certain percentage is allocated to income taxes, a certain percentage to corporation taxes, a certain percentage to liquor taxes, and a certain percentage to consumption taxes, and the entire amount of the Local Corporate Tax is allocated to local governments. There are two types of local allocation tax: the ordinary local allocation tax and the Special Tax Allocation, which is allocated according to special circumstances such as disasters. The ordinary local allocation tax is allocated to local governments whose standard financial requirements exceed their standard financial revenues, based on the difference (shortage of financial resources).

5.2.2 Local Special Grants, etc.

A grant from the national government to local governments, consisting of a special local grant provided to compensate for the decrease in revenue of local governments resulting from the implementation of Special Tax Deduction for Housing Loan and fixed-amount tax cuts (FY 2024 and FY 2025) in the individual residential tax, and a special grant to compensate for the decrease in local tax revenue as a measure against the novel coronavirus infectious disease (COVID-19), provided to compensate for the decrease in revenue of local governments due to the expansion of special measures for fixed asset tax for the realization of a productivity revolution.

5.2.3 local transfer tax

A tax in which tax sources that should be categorized as local taxes are formally collected as national taxes and transferred to local governments.

At present, local transfer tax includes local gasoline transfer tax, special transfer tax, oil gas transfer tax, motor vehicle weight transfer tax, aircraft fuel transfer tax, forest environmental transfer tax, and special corporation project transfer tax.

5.3 Earmarked resources

A source of funds that is earmarked and has fixed costs that can be spent.

5.3.1 Treasury Disbursements

Based on the division of expenses between the national government and local governments, the national government provides local governments with burden charges, commission expenses, subsidies for encouragement of specific measures or financial assistance, etc.

5.3.2 Prefectural Expenditures

Disbursements from prefectures to municipalities. There are two types of disbursements: disbursements that prefectures independently provide to municipalities as their own measures, and disbursements that prefectures provide to municipalities as all or part of their expenses from national treasury disbursements (indirect subsidies).

6. Expenditures (by purpose)

Classification of expenditures focusing on administrative purposes. The expenses of local governments can be roughly divided into general affairs expenses, public welfare expenses, health expenses, agriculture, forestry and fisheries expenses, civil engineering expenses, education expenses, parliamentary expenses, labor expenses, commerce and industry expenses, fire services expenses, public debt expenses, police expenses, etc., according to their administrative purposes.

6.1 General Expenses

Expenses required for general administrative affairs of local governments (finance, planning, management of government buildings, personnel affairs, family registers, tax collection, elections, statistics, etc.) and other expenses that cannot be classified by purpose.

6.2 Public welfare expenses

Local governments are implementing measures such as social welfare improve the equipment, management, and implementation of public assistance for children, the elderly, and persons with disabilities in order to enhance social welfare. Expenses required for these measures.

6.3 Sanitation costs

In order to maintain and improve the health of residents and improve the living environment, local governments promote measures related to medical care, public health, mental health, etc., and implement measures closely related to the daily lives of residents, such as the collection and treatment of general waste such as human waste and garbage. Expenses required for these measures.

6.4 Agriculture, forestry and fisheries expenses

In order to promote the agriculture, forestry and fisheries industries and ensure a stable supply of food, local governments are implementing measures such as the promotion of the sixth industry and the revitalization of farming and fishing villages in a society with a declining population, in addition to existing measures such as the development of production bases, structural improvements, measures for consumption and distribution, and the development and dissemination of technologies related to the agriculture, forestry and fisheries industries. Expenses required for these measures.

6.5 Civil works expenses

Local governments construct and develop public facilities such as roads, rivers, houses, and parks in order to develop regional infrastructure, and maintain and manage these facilities. Expenses required for these measures.

6.6 Education expenses

Local governments carry out educational and cultural administration such as school education and social education in order to promote education and improve culture. Expenses required for these educational measures.

6.7 Parliamentary Expenditure

Expenses required for assemblies of local public entities, in addition to the remuneration of Diet members, personnel expenses for employees of the assembly secretariat, and expenses required for the construction of the assembly hall, etc.

6.8 Labor Costs

In order to improve the welfare of employed people, local governments are taking measures such as the enhancement of vocational ability development, financial measures, and unemployment measures. Expenses required for these measures.

6.9 Commercial and industrial expenses

In order to promote local commerce and industry and strengthen their management, local governments are implementing a variety of measures, including improving the management and technological capabilities of SMEs, promoting local energy projects, attracting enterprises, and implementing consumption and distribution measures. Expenditures required for these measures.

6.10 Fire Fighting Expenses

Local governments provide fire service to protect people's lives, bodies, and properties from disasters such as fires, storms, floods, and earthquakes, to prevent and mitigate damage from these disasters, and to appropriately transport injured and sick people due to disasters. Expenses required for these measures.

6.11 Public debt service

Expenses required for the redemption of principal and interest of local government bonds issued by local governments. While debt service under expenditures by nature is limited to principal and interest redemption of local government bonds and temporary borrowing interest, debt service under expenditures by purpose includes administrative expenses such as issuance fees and discount fees for local government bonds in addition to expenses required for principal and interest redemption.

6.12 POLICE EXPENSES

Prefectures conduct police administration to prevent crime, ensure traffic safety, maintain the safety and order of local communities, and protect the lives, bodies, and property of the people. Expenses required for these measures.

7. Expenditures (by type)

Classification of expenditure with attention to the economic nature of expenses. Expenses of local governments can be roughly divided into mandatory expenses, investment expenses and other expenses according to their economic nature.

7.1 Personnel expenses

Expenses paid to employees, etc. as consideration and remuneration for their work, such as salaries for employees, salaries for special positions, remuneration for members of the Diet, remuneration for various committee members, and retirement allowances.

7.2 subsidy

Expenses related to benefits implemented by local governments based on each type of social security system as part of the laws and regulations and various aid independently conducted by local governments.

Subsidy include not only cash but also expenses required for the provision of goods.

7.3 Public debt service

Expenses required for the redemption of principal and interest of local government bonds issued by local governments.

Public debt service in expenditures by nature is limited to principal and interest redemption of local government bonds and temporary borrowing interest, while public debt service in expenditures by purpose includes administrative expenses such as issuance fees and discount fees for local government bonds in addition to expenses required for principal and interest redemption.

7.4 Ordinary Construction Expenses

Expenses required for the construction, expansion, etc. of public or alternative facilities. Of these, new development refers to the widening of existing roads, bridges, etc., the addition of sidewalks and traffic lanes, and the strengthening of function in existing public facilities, etc., in addition to the construction of new public facilities, etc. Renewal development refers to the earthquake-proofing of facilities, reconstruction or rebuilding due to aging, demolition related to reconstruction, renewal of equipment, etc.

7.4.1 Subsidized Projects

Projects implemented by local governments with contributions or subsidies from the national government.

7.4.2 Parent Business

Projects voluntarily implemented by local governments at their own expense without receiving subsidies, etc. from the national government.

7.4.3 Projects under National Government Jurisdiction

Projects in which the State itself carries out construction projects on roads, rivers, erosion control, ports, etc., and disaster restoration projects for these facilities. The scope of each project is specified by the relevant law. The contribution for projects under the direct control of the State is paid by local governments to cover part of the expenses for projects under the direct control of the State according to the regulations of laws and regulations.

7.5 Non-personnel expenses

A collective term for expenditures of a consumptive nature incurred by local governments other than personnel costs, maintenance costs, subsidy, subsidies, etc. Specific examples include staff travel expenses, equipment purchase costs, commission fees, etc.

7.6 Subsidies, etc.

This includes disbursements to other local governments, the national government, corporations, etc., as well as transfers based on the provisions of Article 17-2 of the Local Public Enterprise Act (Act No. 292 of 1952).

7.7 Others

7.7.1 Disaster recovery project costs

Expenses required to restore facilities damaged by disasters such as earthquakes, typhoons, and other abnormal natural phenomena to their original state.

7.7.2 Maintenance and repair expenses

Expenses required for the maintenance of facilities managed by local governments.

7.7.3 Investments and equity investments

Expenses for acquisition of national and local government bonds, and contributions and subscriptions to the third sector, etc.

7.7.4 Withdrawals

Expenditures between the Ordinary Account and the Public Works Account or between Public Works Accounts. Expenditures to the Fund for the investment of a fixed amount of funds are also included in transfers.

Transfers to public enterprises not subject to the law are also included.

7.7.5 Reserves

Expenses for funds established to maintain property or accumulate funds for a specific purpose.

7.7.6 Loans receivable

Loans provided by local governments to local residents and businesses for various administrative purposes.

8. Contact Information

For inquiries regarding the details of local public finance: Financial Research Division, Local Finance Bureau, Ministry of Internal Affairs and Communications

- Address: 2-1-2 Kasumigaseki, Chiyoda-ku, Tokyo 100-8926

- Phone: 03 5253 5649

9. Related Information

Local public finance

Ministry of Internal Affairs and Communications conducts the Survey on the Financial Status of Local Governments every fiscal year to assess the status of local public finance. Digital Agency is working with Ministry of Internal Affairs and Communications to make information on local public finance more visible and easy to understand.